Bid-Trust has created hundreds of guides and resources to help you learn accounting. These articles are meant to be used as self-study, so you can read and learn at your own pace. In the guides, you’ll see examples and step-by-step instructions on the most important and common accounting principles and concepts required to be a world-class financial analyst.

The revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a company’s financial statements. Theoretically, there are multiple points in time at which revenue could be recognized by companies. Generally speaking, the earlier revenue is recognized, it is said to be more valuable to the company, yet a risk to reliability.

The three financial statements are: (1) the Income Statement, (2) the Balance Sheet, and (3) the Cash Flow Statement. These three core statements are intricately linked to each other and this guide will explain how they all fit together. By following the steps below, you’ll be able to connect the three statements on your own.

If you want a career in accounting, T Accounts may be your new best friend. The T Account is a visual representation of individual accounts in the form of a “T,” making it so that all additions and subtractions (debits and credits) to the account can be easily tracked and represented visually.

In an accounting career, journal entries are by far one of the most important skills to master. Without proper journal entries, companies’ financial statements would be inaccurate and a complete mess.

An easy way to understand journal entries is to think of Isaac Newton’s third law of motion, which states that for every action, there is an equal and opposite reaction. So, whenever a transaction occurs within a company, there must be at least two accounts affected in opposite ways.

For example, if a company bought a car, its assets would go up by the value of the car. However, there needs to be an additional account that changes (i.e., the equal and opposite reaction). The other account affected is the company’s cash going down because they used the cash to purchase the car.

Finally, just like how the size of the forces on the first object must equal that of the second object, the debits and credits of every journal entry must be equal.

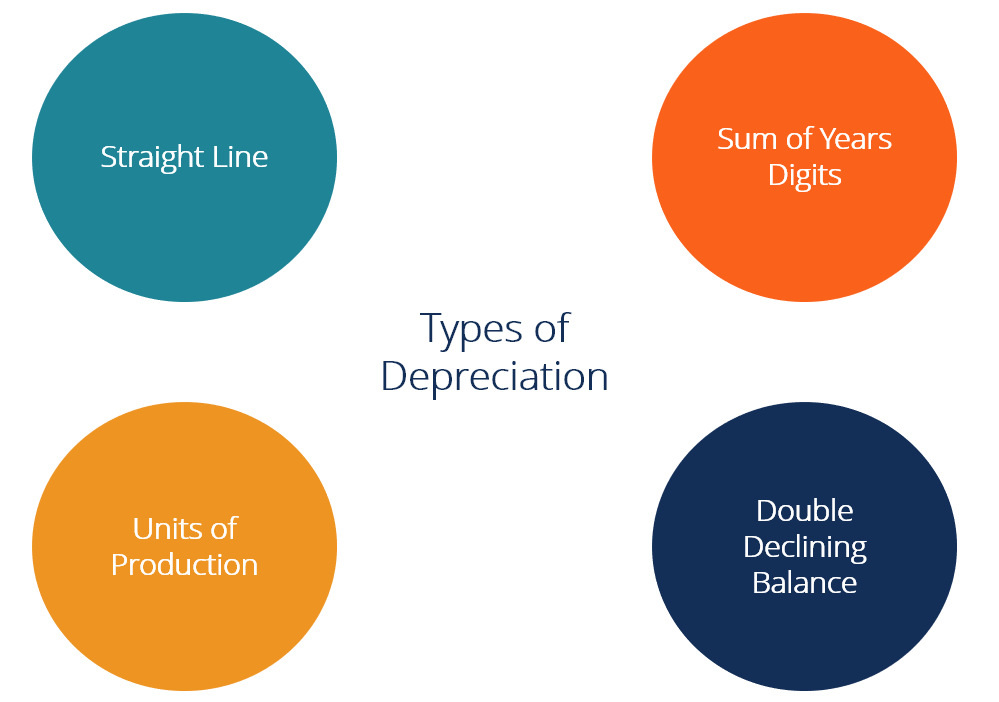

There are several types of depreciation expense and different formulas for determining the book value of an asset. The most common depreciation methods include:

Depreciation expense is used in accounting to allocate the cost of a tangible asset over its useful life. In other words, it is the reduction in the value of an asset that occurs over time due to usage, wear and tear, or obsolescence. The four main depreciation methods mentioned above are explained in detail below.

Copyright © 2021 BID. All Rights Reserved. By Bid-trust.com